|

|

April 15, 2026 Newsletter 249 |

|---|---|

Market Highlight |

|---|

|

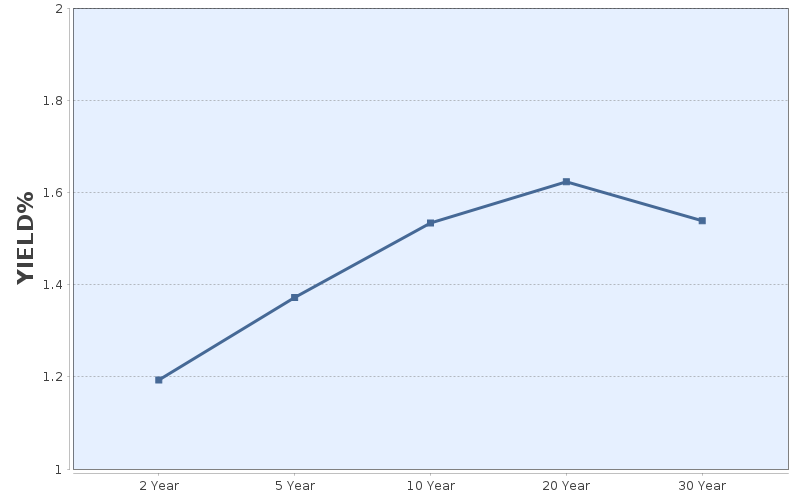

Bond Market In the U.S. bond market, the U.S. February manufacturing purchasing managers index (PMI) reported on March 2 by The Institute for Supply Management (ISM) dropped to 52.4, higher than that of market expectation of 51.5 but lower than that of the preceding month of 52.6. According to the February non-farm payroll and unemployment statistics released by the Bureau of Labor Statistics on March 11, non-farm jobs fell by 92,000, significantly lower than the market expectation of 55,000 new jobs; the January non-farm payroll and unemployment statistics were revised upward from 130,000 jobs to 160,000 jobs; the unemployment rate rose to 4.4% in February, higher than those of market expectations and the preceding month of 4.3%. The February Consumer Price Index (CPI) published by the Bureau of Labor Statistics on March 13 remained comparable to that of the preceding month of 2.4%, which was in line with market expectations. The core CPI in February increased 2.5% over the last 12 months, which was comparable to that of the preceding month of 2.5%, and in line with market expectations. The Fed decided on March 18 to maintain the federal funds rate in the range of 3.50% to 3.75%. Apart from Stephen Miran, a member of the Board of Governor and chairman of the Council of Economic Advisers, who advocated for a further 25-basis-point rate cut, other members voted to keep the interest rates unchanged. The Fed's latest statement added the high risk of uncertainty in the Middle East and revised the description of the unemployment rate from showing “some signs of stabilization” to having “little changed in recent months.” The latest March interest rate dot plot shows that median rates of 2026 and 2027 drop by 25 basis points respectively, with the rate cuts ending in 2028. In terms of economic forecasts, the Fed slightly revised its economic growth forecasts upward for 2026 to 2028 to 2.4% (previously 2.3%), 2.3% (previously 2.0%), and 2.1% (previously 1.9%). Regarding inflation, the Fed slightly revised its core PCE inflation forecasts for 2026 and 2027 upward to 2.7% (previously 2.5%) and 2.2% (previously 2.1%), while maintaining its core PCE inflation forecast for 2028 at 2.0%. Fed Chair Jerome Powell said at a press conference after the meeting that short-term inflation is expected to rise in recent weeks, possibly reflecting the sharp rise in oil prices due to supply disruptions in the Middle East, but mostly long-term inflation is expected to remain in line with the Fed’s 2% inflation target. During March, the yields of U.S. treasures trended upward, mainly due to the military conflict in the Middle East pushing up oil prices, which further fueled inflationary pressures and exacerbated market expectations that monetary policy would remain tight. As of March 31, the yield on the 10-year U.S. Treasury note closed at 4.317%, up 37.9 basis points from the end of February (3.938%).

Major stock exchanges in the world, such as Stockholm Stock Exchange, London Stock Exchange, Luxembourg Stock Exchange, Euronext, Korea Exchange, Hong Kong Exchange, and Singapore Exchange have set up a special board for the trading of sustainable bond, economic, social, and governance (ESG) bond or socially responsible investment (SRI) bond. In a move to promote Taiwan's sustainable finance, continue to keep abreast of international markets and enhance the international visibility of our capital market, and in support of the Corporate Governance 3.0 – Sustainable Development Roadmap, Green Finance Action Plan 3.0 as well as Capital Market Roadmap 2021–2023 promoted by the competent authorities, Taipei Exchange (TPEx), in reference of international trends, integrated the green bond listing and trading mechanism, social bond listing and trading mechanism, and sustainability bond listing and trading mechanism into the sustainable bond listing and trading mechanism and has set up a Sustainable Bond Board. On top of the capital bonds dedicated to sustainable developments, in order to assist enterprises achieve their overall strategic sustainable development goals, work toward net zero emissions and sustainable transformations, as well as to expand the range of sustainable bonds offered in Taiwan, the TPEx has promulgated the Sustainability-Linked Bond (SLB) trading system on July 8, 2022 so as to offer even more diversified sustainable fund-raising and investment tools, as well as to keep abreast of international markets for issuers and investors at home and abroad. Furthermore, to provide the market with well-rounded information and contents on sustainable bonds, the TPEx has formulated a dedicated Sustainable Bond website (https://www.tpex.org.tw/web/bond/sustainability/index.php?l=zh-tw). On top of relevant information such as Taiwan's progress in developing sustainable bonds over the years, summaries on the bonds, overviews on bond issuance (e.g., issuing criteria, issuance plan and post-market report), latest information, and research reports, the website also aims to actively strengthen ESG information disclosure on the bond issuers. "Issuer's Sustainable Development Strategies" and "Sustainable Bond Benefits" sections have been added to the website since 2022. The convenient and user-friendly interface is designed to provide market participants with comprehensive and enriched reference information, thereby allowing them to understand the latest development trends and directions in the sustainable bond market both at home and abroad. |

|

TPEx Treasury Yield Curve

2026 Mar

|

|

15F., No.100, Sec. 2, Roosevelt Rd., Taipei City 100, Taiwan (R.O.C.) Tel : 886-02-2369-9555 For more information please visit our website : https://www.tpex.org.tw/en-us/index.html |