|

|

June 15, 2026 Newsletter 251 |

|---|---|

Market Highlight |

|---|

|

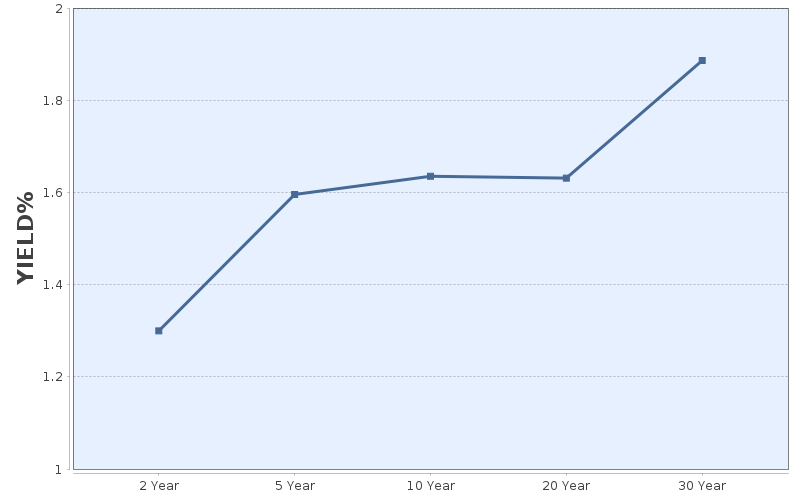

Bond Market In the U.S. bond market, the U.S. April manufacturing purchasing managers index (PMI) reported on May 1 by the Institute for Supply Management (ISM) remained at 52.7, comparable with that of the previous month but lower than market expectations of 53.2. According to the April non-farm payroll and unemployment statistics released by the Bureau of Labor Statistics on May 8, around 115,000 more non-farm jobs were created in April, higher than the market expectation of 65,000 jobs; the March number was revised upward from 178,000 jobs to 185,000 jobs. The unemployment rate in April remained comparable at 4.3% to March, which was in line with market expectations. The April Consumer Price Index (CPI) published by the Bureau of Labor Statistics on May 12 showed an annual increase of 3.8%, higher than market expectations of 3.7% and the 3.3% level in the previous month. The annual core CPI growth rate for April rose to 2.8% from 2.6% in March, higher than market expectations of 2.7%. On May 22, the White House held a swearing-in ceremony for Kevin Warsh, the new chairman of the Federal Reserve (Fed). On the same day, the Federal Open Market Committee (FOMC) unanimously elected Warsh as the 17th chairman of the FOMC. Warsh has stated that he will determine policy and interest rates based on the actual economic situation and promised to bring about institutional changes to the Fed, including shrinking the $6.7 trillion balance sheet, establishing a new inflation analysis framework, and changing the Fed's external communication methods. Fed Governor Christopher Waller said he currently prefers to remain patient and keep interest rates unchanged until the impact of the war becomes clearer, but does not rule out the possibility of future rate hikes if inflation fails to cool down quickly. In his speech, he stated, “Based on this recent data, I would support removing the ‘easing bias’ language in our policy statement to make it clear that a rate cut is no more likely in the future than a rate increase.” The U.S. Treasury yields initially rose and then fell in May. In the middle of the month, higher-than-expected April inflation and retail sales data, coupled with a stable labor market, increased market expectations for further tightening of monetary policy by the Fed, driving up yields. In addition, weak demand at auctions of 3-, 10-, and 30-year U.S. Treasury bonds also put upward pressure on yields. However, subsequent progress in the U.S.-Iran peace talks eased market concerns about energy supply risks, leading to a decline in oil prices. Furthermore, lower-than-expected U.S. Q1 GDP and core Personal Consumption Expenditure Price Index (PCE Index) data prompted the market to reassess the outlook for monetary policy, pushing yields down from their highs. As of May 31, the yield on the 10-year U.S. Treasury note closed at 4.436%, up 6.5 basis points from the level at the end of April (4.371%). In the European bond market, market research firm S&P Global reported on May 4 that the final value of Eurozone manufacturing PMI for April was 52.2, higher than the level of the preceding month of 51.6. Eurostat released its final Eurozone CPI annual growth rate for April of 3.0% on May 20, which was higher than that (2.6%) of the month earlier. The final reading for the core CPI annual growth rate was 2.2%, lower than the previous month's 2.3%. European Central Bank (ECB) President Christine Lagarde said policymakers are expected to raise the inflation outlook when they meet next month. Lagarde, however, did not elaborate further on whether the adjustment to the inflation outlook meant the ECB would raise interest rates in June. She stated that the current situation is extremely uncertain. They must examine all available data, assess the economic trajectory for the next few quarters, determine whether any action is necessary, and evaluate the medium-term impact. In May, yields on major European government bonds initially rose and then fell. In the middle of the month, concerns about inflation intensified due to the ongoing tensions between the U.S. and Iran, and rising oil prices, which drove up the yields of major European government bonds. In addition, the UK Prime Minister faced pressure to step down due to defeat in local elections, and the market was worried that subsequent fiscal policies would become more expansionary, pushing up the yields of UK government bonds and leading to a rise in the yields of major European government bonds. However, subsequent progress in U.S.-Iran negotiations eased market concerns about energy supply risks, leading to a decline in oil prices. In addition, the gradual stabilization of the UK political situation caused the yields on major European government bonds to fall from their highs. The yields of German, French, and Italian 10-year government bond as of May 31 closed at 2.938%, 3.549% and 3.652% respectively, down 9.9bps, 14.4bps and 20.7bps from the end of April. Domestically, the April Taiwanese economic indicators published by the National Development Council on May 28 showed that the latest economic composite score was 39, comparable to that of the preceding month, while the economic monitoring indicator continued to flash red. According to the import/export data published by the Ministry of Finance on May 8, the exports in April reached US$67.62 billion, the second highest over any given month in the past, up 39.0% compared with that of the same period last year (an increase of 34.6% in NTD terms). Taiwan government bond yields rose in May, mainly due to the lower-than-expected results of the 2-year bond auction, which led to higher yields. As of May 31, the 10-year Taiwan government bond yield closed at 1.6350%, up 13.25 basis points from the end of the previous month. The 5-year and 10-year benchmark government bond yields closed at 1.5955% and 1.6350%, respectively, as of May 31 (as compared to 1.3800% and 1.5025% at the end of April). The daily turnover in the NTD bond market averaged NT$144.491 billion for the month of May 2026. The daily average of outright trade amounted to NT$12.750 billion (8.82%) and that of RP/RS trade was NT$131.741 billion (91.18%). The daily average of market turnover increased 3.95% as compared to that of April (while the daily market turnover in April averaged NT$139.001 billion; it amounted to NT$8.065 billion (5.80%) for outright trade and NT$130.936 billion (94.20%) for RP/RS trade). Major stock exchanges in the world, such as Stockholm Stock Exchange, London Stock Exchange, Luxembourg Stock Exchange, Euronext, Korea Exchange, Hong Kong Exchange, and Singapore Exchange have set up a special board for the trading of sustainable bond, economic, social, and governance (ESG) bond or socially responsible investment (SRI) bond. In a move to promote Taiwan's sustainable finance, continue to keep abreast of international markets and enhance the international visibility of our capital market, and in support of the Corporate Governance 3.0 – Sustainable Development Roadmap, Green Finance Action Plan 3.0 as well as Capital Market Roadmap 2021–2023 promoted by the competent authorities, Taipei Exchange (TPEx), in reference of international trends, integrated the green bond listing and trading mechanism, social bond listing and trading mechanism, and sustainability bond listing and trading mechanism into the sustainable bond listing and trading mechanism and has set up a Sustainable Bond Board. On top of the capital bonds dedicated to sustainable developments, in order to assist enterprises achieve their overall strategic sustainable development goals, work toward net zero emissions and sustainable transformations, as well as to expand the range of sustainable bonds offered in Taiwan, the TPEx has promulgated the Sustainability-Linked Bond (SLB) trading system on July 8, 2022 so as to offer even more diversified sustainable fund-raising and investment tools, as well as to keep abreast of international markets for issuers and investors at home and abroad. Furthermore, to provide the market with well-rounded information and contents on sustainable bonds, the TPEx has formulated a dedicated Sustainable Bond website (https://www.tpex.org.tw/web/bond/sustainability/index.php?l=zh-tw). On top of relevant information such as Taiwan's progress in developing sustainable bonds over the years, summaries on the bonds, overviews on bond issuance (e.g., issuing criteria, issuance plan and post-market report), latest information, and research reports, the website also aims to actively strengthen ESG information disclosure on the bond issuers. "Issuer's Sustainable Development Strategies" and "Sustainable Bond Benefits" sections have been added to the website since 2022. The convenient and user-friendly interface is designed to provide market participants with comprehensive and enriched reference information, thereby allowing them to understand the latest development trends and directions in the sustainable bond market both at home and abroad. |

|

TPEx Treasury Yield Curve

2026 May

|

|

15F., No.100, Sec. 2, Roosevelt Rd., Taipei City 100, Taiwan (R.O.C.) Tel : 886-02-2369-9555 For more information please visit our website : https://www.tpex.org.tw/en-us/index.html |